Australian Invoice Finance managing director Greg Charlwood discusses why invoice finance may help businesses smooth out uneven cash-flow.

Late payment of invoices is a major problem for small-to-medium enterprises (SMEs) in the Australian rag trade, which can even lead to the closure of businesses in extreme cases.

At the very least, it creates uneven cash flow, potentially leading to problems paying suppliers and staff, missed opportunities and falling behind in tax payments.

Research from illion for the 2019 June quarter revealed that one third of Australian SMEs (which it defines as businesses with less than 500 employees) experience problems with late payment of invoices.

The problem becomes worse around Christmas and New Year, when clients and customers in the rag trade often shut down for an extended period.

The illion research showed that the textile, clothing and footwear industries are exposed to sectors with some of the worst track records of late payments.

Retail, for example, topped the late payments list with an average late payment time of 12.9 days. That’s six weeks that it takes suppliers to be paid, on average.

The manufacturing sector recorded an average late payment time of 11.8 days while wholesale was at 10.7 days.

How can you protect your business from late payments?

Invoice finance (also known as debtor financing, factoring, cash-flow finance and invoice discounting) is simply a line of credit against the receivables of a business that helps smooth out uneven cash flow.

It enables businesses to convert their unpaid invoices to cash by leveraging their accounts receivable, typically one of the largest assets on a business’ balance sheet.

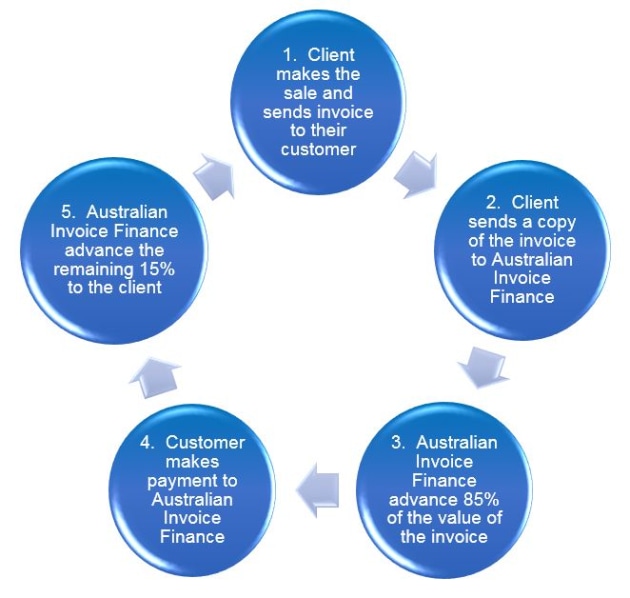

Under the invoice finance process, up to 90% of the value of an outstanding invoice is converted to cash, usually within 24 hours.

Once the outstanding invoice is paid, the remaining 10% of the value of the invoice, less a service fee of around 2%, is paid to the company.

The invoice finance process

There are three main reasons why businesses should consider invoice finance for cash flow management.

Firstly, the finance landscape has changed: there is a lack of competition among Australian small business lenders and businesses are finding it increasingly difficult to rely on banks for financing.

Secondly, as a result of subdued economic conditions, many businesses have encountered cash-flow shortages that have significantly impacted their operations and growth opportunities.

And finally, SMEs don’t want to risk personal property to secure finance.

Unlike other forms of credit, invoice finance is based on invoices and does not require personal property such as the family home as security.

An invoice financing facility may also include a sales ledger management service that can issue statements on a regular basis, handle cash allocations, collect outstanding payments and maintain detailed accounts of a business’ transactions.

This can help small businesses reduce costs and free up management time to focus on strategic issues and business development.

It’s a good idea to speak to at least a couple of invoice finance providers prior to signing a contract to ensure that partnership is a good fit.

Clients should also be prepared to answer questions from potential invoice finance providers such as:

• What type of business are you in? – Invoice finance providers often prefer to deal with businesses selling a product or service which can easily be shown to have been provided e.g. by a signed delivery note or timesheet. The rag trade is well suited to invoice finance in this regard.

• What debtors do you have? – Invoice finance providers will want to understand the quality and spread of a client’s debtors before entering into an arrangement. They will also typically enquire about a business’ bad-debt record, the age of the sales ledger and overall collection performance.

• How good is your record keeping? – Any provider of invoice finance will want to ensure that invoices can be easily followed through the collection process.

To find out more about Australian Invoice Finance, check out their website at www.austif.com.au